Retirement planning can feel like a moving target.

Many people wonder whether they are saving enough, making the right decisions, or preparing adequately for the future. The challenge is that retirement readiness is not determined by a single number or milestone.

Instead, it is often the result of many factors working together. Savings habits, lifestyle goals, income sources, healthcare planning, and timing all play a role.

If retirement is on your horizon, one of the most valuable exercises is stepping back and asking a simple question:

Am I on the right track?

The answer often begins with reviewing a few key areas of your financial life.

Before reviewing account balances or investment statements, it helps to think about what retirement means to you.

Retirement looks different for everyone.

Some people plan to travel frequently. Others want to spend more time with family, volunteer, pursue hobbies, or continue working in a reduced capacity. Some envision staying in their current home, while others plan to relocate.

Your vision for retirement influences nearly every financial decision that follows.

Ask yourself: What do I want my retirement years to look like?

Having a clear picture can help provide context for the rest of your planning.

Many people focus heavily on how much they have already saved. While current savings matter, your habits are often just as important.

Are you contributing consistently toward retirement?

Have contributions increased as income has grown?

Do your current savings habits reflect the importance of your long-term goals?

Retirement planning is often built through consistency over many years. Reviewing your habits can help you understand whether your actions align with your intentions.

Progress is rarely the result of one decision. It is often the outcome of many small decisions repeated over time.

One of the most important parts of retirement planning involves understanding future spending needs.

Retirement often changes how money is spent, but it does not eliminate expenses altogether.

Housing, healthcare, travel, taxes, and lifestyle activities all continue to play a role. Some expenses may decrease while others increase.

Rather than trying to predict every detail, focus on broad categories and priorities.

What expenses are likely to remain important? Which ones may change?

Thinking through these questions can help create a more realistic picture of retirement readiness.

Retirement income often comes from multiple sources.

Social Security benefits, retirement accounts, pensions, investment income, and other assets may all contribute to your overall income strategy.

Understanding where future income may come from helps create greater confidence around retirement planning. This is also a good opportunity to identify areas that may deserve additional attention or review.

The goal is not to predict exact outcomes. It is to understand how different income sources may work together over time.

Retirement planning becomes more focused as your timeline becomes clearer.

For some people, retirement is five years away. For others, it may be ten or fifteen years away. Some may plan for a gradual transition rather than a specific retirement date.

Your timeline affects savings decisions, investment strategy, and future planning priorities.

Ask yourself: Has my desired retirement timeline changed in recent years?

Life circumstances, career satisfaction, health, and family considerations can all influence the answer.

Reviewing your timeline periodically helps ensure your plan continues to reflect your goals.

Healthcare is one of the most common concerns people have when preparing for retirement.

Medical expenses can change over time, and healthcare needs often evolve as people age.

While no one can predict future healthcare costs with certainty, retirement readiness should include conversations around healthcare coverage, potential expenses, and how those costs fit into your broader financial picture.

Considering healthcare as part of retirement planning helps create a more complete view of the future.

Retirement planning extends beyond savings and income.

As retirement approaches, it can be helpful to review beneficiary designations, wills, powers of attorney, and other estate planning documents.

These items are easy to overlook but often play an important role in ensuring your plans reflect your wishes.

Life changes such as marriage, divorce, births, deaths, or family transitions may create a need for updates over time.

Regular reviews help keep important documents aligned with your current situation.

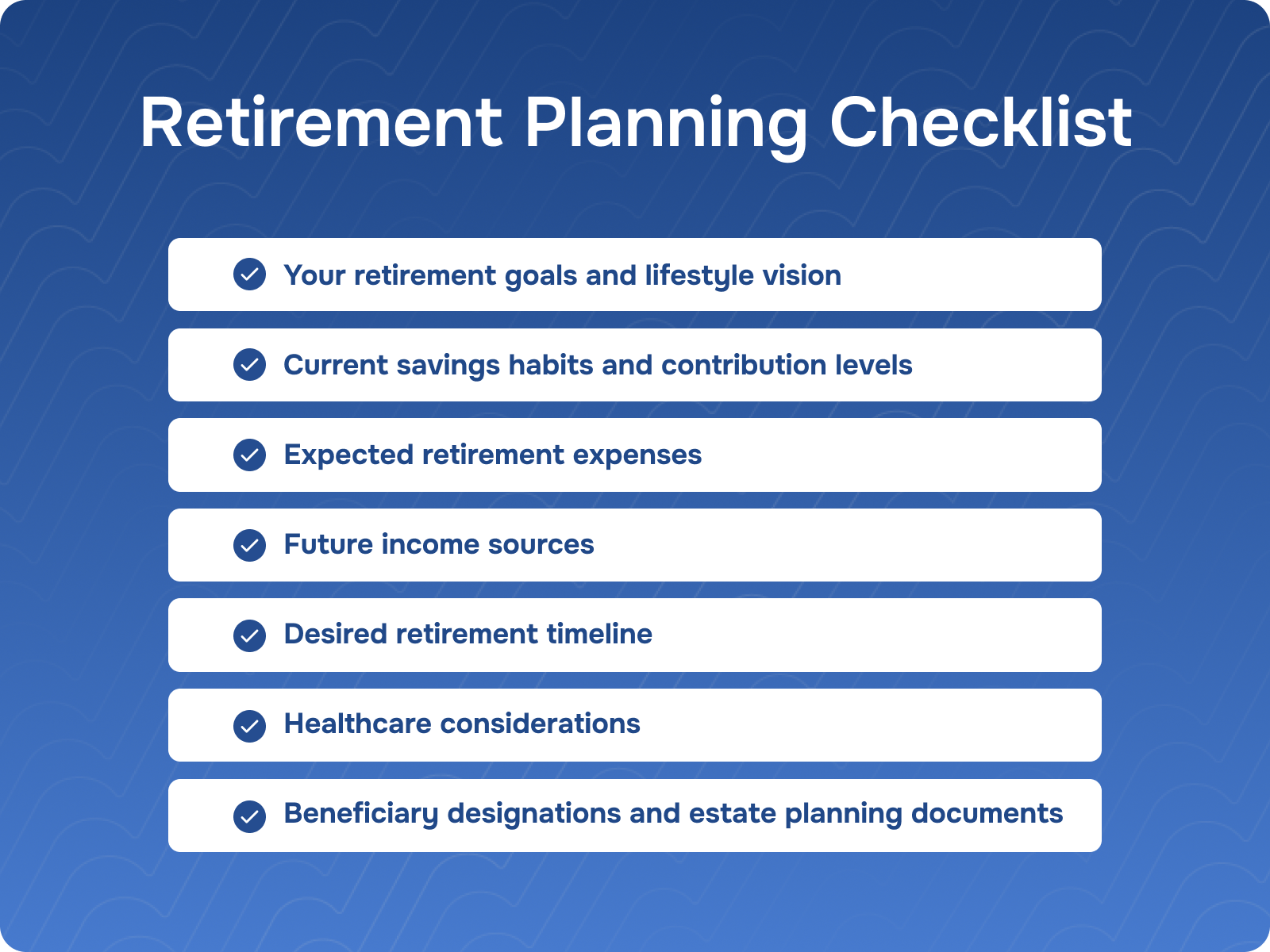

If you are evaluating your retirement readiness, consider reviewing the following areas:

You do not need every answer immediately. The purpose of a retirement planning checklist is to help identify areas worth exploring.

Retirement planning involves many moving parts. Some people prefer to manage the process independently, while others find value in working with a financial advisor.

A financial professional can help you review your retirement readiness, organize information, and evaluate how different planning decisions work together.

Highland Trust Partners works with individuals and families in Athens, Georgia and across the United States, helping them navigate retirement planning with clarity and perspective.

Many people approach retirement planning looking for certainty. In reality, retirement readiness is often about preparation rather than prediction.

The most productive question may not be whether you have done everything perfectly.

It may be whether you are making thoughtful progress toward the future you want.

By reviewing your goals, evaluating your plan, and staying engaged with the process, you can build greater confidence in the path ahead.

More than 99% customer satisfaction is our success.

The expertise and dedication of this team have been game-changers for our business. Highly recommended! Outstanding service! Their innovative approach helped us achieve measurable success in record time

From start to finish, the team provided unparalleled support. They truly understood our needs and delivered results that surpassed our expectations.

The team at exceeded our expectations with their strategic insights and innovative solutions. Their professionalism and dedication to our success were truly remarkable.

Thanks to Casho, we streamlined our operations and achieved our growth goals. Their hands-on approach and expertise made a real difference for our business

From day one, Casho demonstrated professionalism and a genuine commitment to our success. Their innovative approach helped us reach new heights