Many parents begin thinking about education planning soon after their children are born. Others start when school begins to feel closer. No matter when the idea surfaces, one question tends to follow quickly.

How will we prepare for future education costs?

Planning for education costs does not require perfect timing or a complicated strategy. It begins with understanding your goals, your options, and how education savings fit within your overall financial life.

With a thoughtful approach, education planning can feel more manageable and less overwhelming.

Education costs continue to rise over time. Tuition, housing, books, and other expenses can add up quickly once a child reaches college age.

Many families begin saving early because time allows smaller contributions to grow gradually. Starting early is helpful, though planning later can still make a difference.

Education planning is not only about saving money. It also helps families understand what role education funding may play within their broader financial goals.

When parents see how education planning fits into the bigger picture, decisions often feel clearer.

Education planning begins with a simple question.

What type of education experience do you want to prepare for?

Some families plan with the assumption that their child may attend a public university. Others consider private schools, out-of-state programs, or specialized training.

You do not need a perfect answer today. Even a rough estimate helps shape the planning process.

Understanding your general goal allows you to begin estimating potential education costs and determining how savings may support those goals over time.

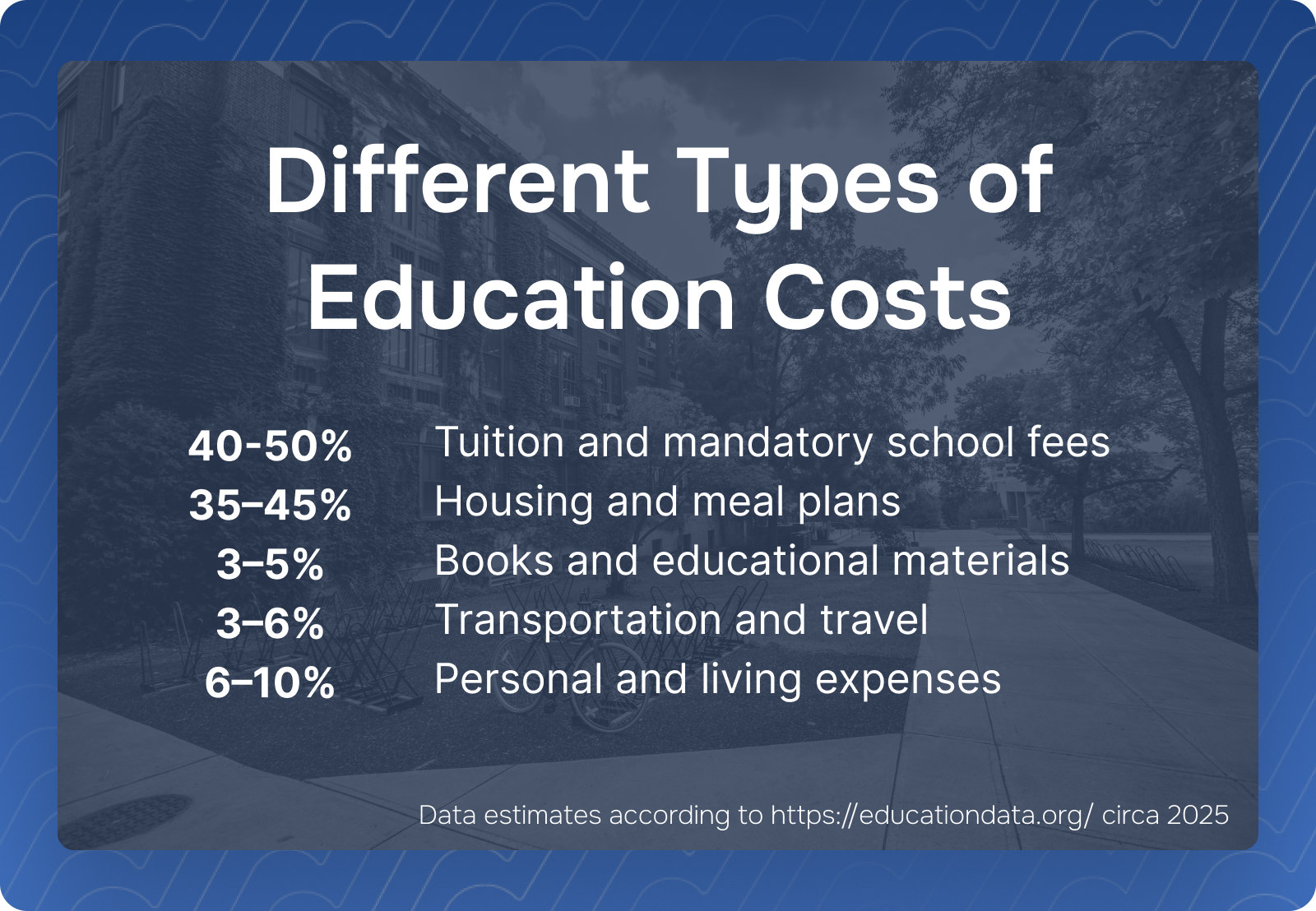

When parents think about education expenses, tuition often comes to mind first. In reality, education costs extend beyond tuition alone.

Families may encounter several types of expenses, including:

Seeing the full picture can help families plan more realistically. It also helps prevent surprises when the time arrives.

Planning for education costs works best when families consider the entire experience rather than focusing on one category.

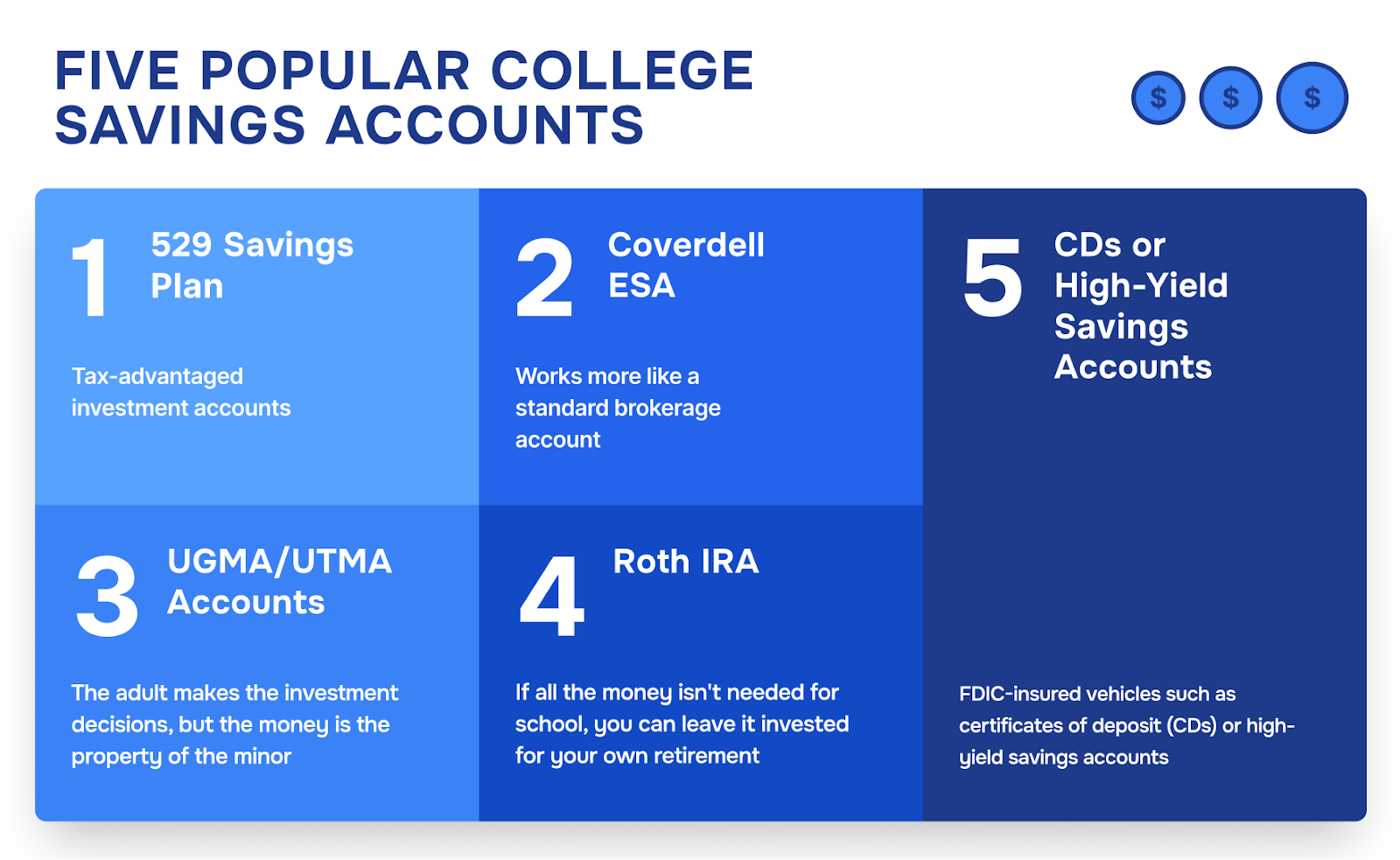

Many parents explore education savings accounts designed to support long-term education planning.

In the United States, one common tool is the 529 education savings plan. These accounts allow families to contribute funds that may grow over time and be used for qualified education expenses.

Each state offers its own version of these plans, though families are not limited to their home state’s program.

Some families also use custodial accounts or other investment strategies to support education savings. Each option carries different rules, tax considerations, and flexibility.

Understanding these choices can help parents determine which approach aligns with their goals.

One of the most important aspects of education planning is balance.

Parents often want to provide opportunities for their children while still protecting their own long-term financial well-being.

Education planning works best when it exists alongside other priorities such as retirement planning, emergency savings, and household stability.

When families view education savings as part of a broader financial plan, they can make decisions with greater clarity.

The goal is not to fund every possible expense. The goal is to create a thoughtful strategy that supports both your child’s future and your own financial security.

Many parents assume they must save large amounts to make education planning worthwhile. In practice, small and consistent contributions can still build meaningful savings over time.

Regular contributions help families develop healthy financial habits. They also allow savings to grow gradually as children move through school.

Consistency often matters more than the exact amount.

Even modest contributions made consistently over many years can help reduce the financial pressure families may feel later.

As children grow, their interests and potential paths may change. Your financial situation may also evolve over time.

For this reason, education planning benefits from periodic review.

Families often revisit their plan when children reach new milestones such as starting middle school, entering high school, or preparing for college applications.

A review can help ensure savings strategies still reflect current goals and financial priorities.

This step helps families stay flexible rather than locked into assumptions made years earlier.

Education planning is not a single decision. It is a process that develops over time.

Parents may begin with simple savings goals and refine their approach as their children grow older. Questions about financial aid, scholarships, and school choices often emerge later in the journey.

Starting the conversation early helps families feel more prepared as those decisions approach.

Even small steps today can make future planning feel less stressful.

Some families prefer to manage education planning on their own. Others find it helpful to speak with a financial advisor who can provide structure and perspective.

A financial professional can help parents understand how education savings interacts with other financial goals, including retirement and long-term planning.

Highland Trust Partners works with individuals and families in Athens, Georgia and across the United States, helping them organize financial priorities and plan for important milestones such as education.

Planning for education costs often begins with a simple intention. Parents want to create opportunities for their children.

Education planning helps turn that intention into a thoughtful strategy. By understanding costs, exploring savings options, and building consistent habits, families can approach the future with greater clarity.

The process does not need to be perfect. It only needs to begin.

More than 99% customer satisfaction is our success.

The expertise and dedication of this team have been game-changers for our business. Highly recommended! Outstanding service! Their innovative approach helped us achieve measurable success in record time

From start to finish, the team provided unparalleled support. They truly understood our needs and delivered results that surpassed our expectations.

The team at exceeded our expectations with their strategic insights and innovative solutions. Their professionalism and dedication to our success were truly remarkable.

Thanks to Casho, we streamlined our operations and achieved our growth goals. Their hands-on approach and expertise made a real difference for our business

From day one, Casho demonstrated professionalism and a genuine commitment to our success. Their innovative approach helped us reach new heights